Why It’s Time to Embrace Digital Lending

Learn how digital lending trends, along with high borrower expectations, make loan origination an essential part of your digital banking strategy.

Lending is a considerable revenue source for many institutions, so ensuring a seamless experience is critical. Outdated technology and inefficient processes hamstring your institution against a shifting economy. And a lackluster or incomplete digital lending experience may drive customers elsewhere.

Most institutions have expanded their digital banking capabilities, recognizing consumers’ shifting preferences and desire for convenience. But in digital lending, slow-moving institutions face a disadvantage.

This blog explores the advantages of a modern digital lending system, providing insight into how your institution can balance digital capabilities without losing sight of your relationship-focused approach to service.

Want to learn more about digital lending? Register for our webinar on Wednesday, August 14 at 1 p.m. CT to explore the latest advancements in modern lending.

What is Digital Lending?

While some may think digital lending is primarily associated with automating the beginning of the lending process, it involves digitizing the entire lending journey in a well-orchestrated process from start to finish. This approach allows your institution the convenience and speed of a digital experience while still enabling you to deliver personalized service, a hallmark of community banks.

It may seem like embracing digital lending requires giving up that valuable human element, but it doesn’t have to be the case. Digital lending allows your bank to increase visibility and automate tasks that were once manual—without automating entire processes.

The trick is to relinquish the right type of control for your institution and use these tools to create a more efficient process. Enhancing your lending capabilities with digital tools helps you avoid delivering an incomplete digital experience that may drive customers elsewhere.

Ideally, your system should support the ability to complete the entire lending process from application to booking without ever needing to step into a branch, streamlining the process for the digitally inclined and affording you opportunities to reach more customers.

Digital lending provides speed and convenience for customers and employees.

Traditional vs. Digital Lending

When you think of the traditional lending process and related technologies, it’s likely that a complex system with disjointed tools and an overwhelming number of input points comes to mind. Traditional lending for many banks involves paper applications and loan worksheets, resulting in a time-consuming, tangled process.

Many institutions also rely on disparate systems, making it difficult to achieve full visibility into the loan origination process. Duplicate data entry adds to the complexity, as institutions manage multiple platforms and places to input data.

As discussed earlier, digital lending streamlines the entire process from start to finish. This holds true for various types of loans, including commercial, consumer or mortgage loans. Instead of re-keying data into multiple tools, an end-to-end loan origination system (LOS) allows bankers to enter data in one time and then supports the flow of this data throughout the process. A LOS also reduces regulatory complexity by proactively identifying potential triggers and requiring specific actions to be taken, such as the delivery of a disclosure to a borrower.

Why Should Banks Modernize Loan Origination?

As competition with big banks and online banks grows increasingly fierce, community banks are under constant pressure to become more efficient. In lending, navigating a complicated process with multiple reporting sources and outdated technology doesn’t lead to many efficiencies. Since lending drives revenue for many community banks, incremental improvements in loan origination can have massive returns on the income statement.

Interest rates and evolving consumer preferences have also led to shifting lending demands over the years. These trends, along with intensified competition and high borrower expectations, make loan origination an essential component of your digital banking strategy.

Further, a modern, centralized lending platform gives employees a holistic look at the process, providing insight into the flow, progress and potential closing times for loans.

According to the ICBA, community banks provide about 60% of all small business loans and more than 80% of agricultural loans. However, it often takes a lot of time and resources to originate these loans, and national banks have more resources to expend. Fortunately, a modern lending system helps level the playing field.

Since lending is a significant revenue source, community banks should develop a digital lending strategy.

Exploring Digital Lending Trends

Recent years have seen the development of new technology, growing competition and high borrower expectations—all leading to an evolution of lending. To navigate this new lending landscape, community banks should consider several trends and factors when implementing a modern, end-to-end lending platform.

Centralized Platform: A modern lending platform provides a streamlined view for your bank, so banks no longer need to rely on multiple spreadsheets and disjointed tools to guide lending processes.

APIs and Integrations: API enablement for real-time integrations creates countless efficiencies, eliminating duplicate data entry. Real-time integration also streamlines processes and frees up staff to work on other tasks rather than devoting all of their time to manually originate loans.

Loan Marketplaces: By connecting bankers across the country to enable loan participations, a loan marketplace provides an opportunity for banks to diversify their portfolio, increase income and supplement their existing balance sheet strategy.

Process Automation: With process automation, banks use APIs to complete work that would otherwise involve manual processes or tasks. Process automation can reduce the amount of effort it takes to complete certain steps within a defined process—such as lending—and result in increased productivity, lower operating costs and reduced delivery time to customers.

The Advantages of Digital Lending

Embracing a modern platform transforms your institution’s approach to lending by streamlining the process and helping you keep pace with consumer expectations. Here are a few ways that digital lending benefits your institution:

Improved User Experience: A variety of companies vie for your customers and brick and mortar banking isn’t for everyone. A configurable lending platform integrated into your core empowers customers to apply for needed funds at their convenience without visiting a branch or turning to another provider. Digital lending also improves the back-end experience for banks, improving lender responsivity. With a centralized platform, banks can create and distribute loans or transfer information to the core system without navigating disparate programs. If you must repeat the loan process, automation does so within seconds.

Efficiency Gains: Digital lending streamlines the lending process and compliance while also providing quick resolutions to requests. By implementing a more efficient process, your institution will experience quicker timelines for everything from application to funding to request resolutions—all while reducing abandonment.

Insight from Analytics: While big banks have leveraged data to gain market share, many community banks have been slower to embrace this strategy. As customer acquisition costs continue to rise, your institution must drive traffic via digital channels. A robust solution can also show what products customers are using, providing lenders with this insight.

Strengthen Regulatory Compliance: Digital lending enhances regulatory compliance by making data more accessible, thus reducing the need for manual searches and minimizing the risk of human error. These platforms provide a comprehensive audit trail for regulatory review, and automation ensures a more consistent compliance environment. Additionally, by streamlining lending processes and reducing the number of platforms used, institutions can simplify risk management and due diligence efforts.

A modern loan origination solution streamlines the lending process while allowing banks to maintain their customer-first approach.

Reimagining the Loan Origination Process

To stay relevant, institutions must embrace digital technologies, even though this shift may alter workflows and require some level of automation and change acceptance. When implementing new technologies, banks should reassess their loan processing methods, focusing on the reasons behind their current processes rather than simply replicating existing methods.

From upfront costs to preexisting vendors, digital lending adoption presents some challenges. You can offset these concerns by embracing automated loan origination tools with the right digital lending strategy for your bank. Altogether, you’ll provide your customers with the service they need and improve your own processes.

Want to learn more about modernizing your lending system and increasing efficiencies? Download our white paper today.

Hawthorn River Lending Regulatory Compliance

Join us to learn more about leveraging technology in Hawthorn River to support your lending process and its regulatory compliance.

Join us to learn more about leveraging technology in Hawthorn River to support your lending process and its regulatory compliance. From 1071, TRID, HMDA, CRA and more in the sea of regulatory acronyms, our end-to-end loan origination solution creates efficiency for financial institutions. Join this session for an overview of the platform, an interactive Q&A and information about:

Transaction data collection

Portfolio level reporting

Loan Policies and more

With more than 23 years in the banking industry, Jennifer Foraker leverages her expertise in lending to support clients utilizing Hawthorn River. As a former loan operations manager with experience from small to large community banks, managing the loan origination for all lines of lending including portfolio management.

Speakers

Jennifer Foraker

Unlocking Efficiencies: The Case for Modernizing Your Community Bank's Lending Platform

Since lending is a considerable revenue source for many institutions, ensuring a speedy, convenient and simple lending process to satisfy customers and support employees is critical. While borrowers expect digital engagement, they also seek a level of personalized service. Bridging the digital divide in the lending process while remaining relationship-focused will help differentiate your bank.

This white paper will explore current challenges in lending, new technologies driving change, the benefits of a centralized lending platform and considerations for banks as they embark on their modern lending journey.

Unlocking Success in Community Bank Lending: Challenges, Opportunities and Modern Solutions

Discover how community banks are seeing success by embracing a simplified lending process with Hawthorn River.

Join us for an insightful webinar exploring the fundamental aspects driving community bank lending. During this webinar, you will:

Explore compliance and regulatory challenges, alongside opportunities in risk management

Learn about the latest advancements in modernizing community lending, such as digital platforms and automated loan processing

Take away valuable insight and strategies for navigating the evolving landscape of community bank lending

Speakers

Jennifer Foraker: Senior Manager of Customer Service - Hawthorn River, CSI

Nate Frost: Solution Specialist - Hawthorn River, CSI

Roxy Salleme: Marketing Specialist II, CSI

Dodd-Frank 1071 - We Are Ready!

Let’s Calm the Hysteria.

Not a week goes by at Hawthorn River without a customer or prospect asking, “where are you with 1071?”. This is such an important topic but also one that receives a lot of hype from consultants, software firms, and industry associations. Phrases like “major investment” and “complex implementation” have littered the social media landscape. Why? Because, as with most regulatory changes, there is a new revenue stream, and everyone wants a piece of the pie.

While we do not sugarcoat the reality that a process change is in order and adoption of the final Dodd-Frank 1071 ruling will require extra effort, we are committed to equipping our customers with the software tools to be successful. No, this is not an add-on “upgrade” that requires a huge budget for our customers. Rather, we have already started deploying compliant 1071 functionality to our customers as part of our standard offering because we were founded for one purpose - To help community bankers THRIVE!

Uncertainty Fuels Chaos.

Prior to the final ruling (and even afterwards), there was considerable uncertainty about the requirements and impact on each institution. Our focus on the topic intensified late last year when a customer contacted us with material concerns after attending an ABA webinar titled “1071 Readiness”. During this webinar, participants were encouraged to begin planning for 1071 at once, to set aside budget dollars, and to lean on their software vendors to take action. Shortly following, customers began contacting us with statements like:

“I understand it’s similar to HMDA, but we are not HMDA reportable so it’s all new to me.”

“My commercial lenders have never had to deal with this nor have their customers.”

“In 2022, I would have had 3x more 1071 Loans than HMDA loans, how will I manage this?”

“I am going to need to hire 2-3 people to support the 1071 data collection process.”

“People can handle bad news and people can handle good news but what people cannot handle is no news.”

Alignment = A Path Forward.

The events above shined a spotlight on the significant levels of anxiety, uncertainty, and concern in the industry, leading us to form our 1071 beta group in March of this year. This beta group, which is made up of seven Hawthorn River customers, was tasked with clarifying the 1071 requirements and prioritizing our development efforts so we could deliver an effective and impactful solution. The first beta group meeting, for lack of better words, was a cluster - each bank had formed its own perceptions and approaches, but none felt confident. Over time, however, we successfully closed the alignment gap and were able to set our sights on an unobstructed vision.

One specific area we continually saw misunderstanding was with the 1071 Reporting Tiers. Many customers had either misinterpreted their reporting tier and/or the timing of when the reporting tier started. Based on our analysis, Hawthorn River has (1) Tier 1 customer, (5) Tier 2 customers, and over (90) Tier 3 customers. This means most of our customers will not need to start collecting data until 2026. But we didn’t want to see the anxiety persist, so Hawthorn River deployed the initial 1071 functionality in the Summer Release with full support for 1071 demographic data collection and reporting coming later this year (more on this topic below).

We encourage all banks to review the following table published by the CFPB to understand when they must report.

Ahead of the Curve.

Yes, it’s true - Community banks that utilize a traditional lending process (e.g. Word, Excel, Email) rather than an end-to-end Loan Origination Solution (LOS) will find it extremely challenging to adopt the necessary processes and systems to comply with Dodd-Frank 1071. With the highly prescriptive CFBP Data Points Chart requiring over 80 unique data outputs for qualified loans, complying with the requirements would likely require dedicated staff, one heck of a spreadsheet, and significant ongoing data reviews/scrubs.

Hawthorn River customers, on the other hand, have a significant head-start because the foundation is already in place. By leveraging our once n’ done data entry philosophy, much of the data requirements for 1071 are already part of the existing system while new data elements are being added using experiences and patterns that lenders already love. This starting point creates a major advantage for our customers by greatly reducing the effort and investment required to comply.

As noted above, The Hawthorn River Summer Release included the first iteration of our Dodd-Frank 1071 support. While there are slight variances in the specific data collection and reporting requirements between HMDA and 1071, the overall process is conceptually the same. The following section outlines the 1071 process along with how Hawthorn River is supporting each step.

Step 1: Identify Loan as 1071

New Configurations have been incorporated to flag when a loan is 1071 eligible (see highlighted section of image below).

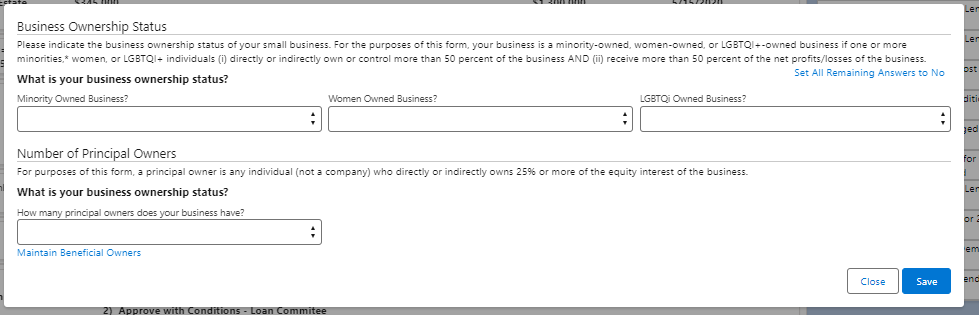

Step 2: Collect Business Ownership Information

A new form has been added to collect the Business Ownership Status information. This data collection is based on the CFPB 1071 Sample Form.

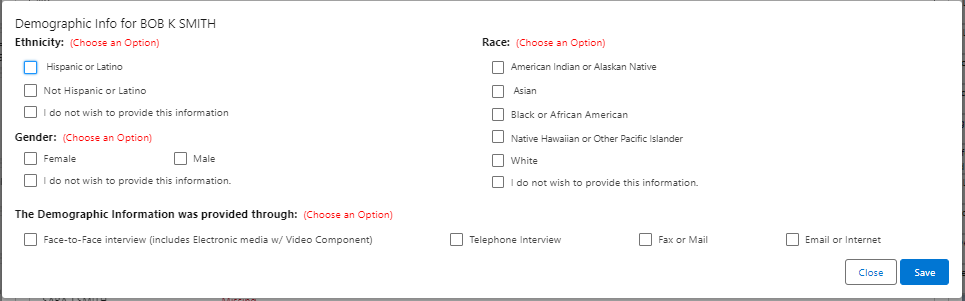

Step 3: Collect Demographic Information on Principal Owners

In our Fall Release, the demographic data collection screens for the principal business owners will be delivered. The screen will closely resemble our HMDA Demographic Screens but will have minor differences based on the 1071 requirements. The screen below is from our current HMDA demographic screen, which expands for additional sub-options based on the selection. These sub-options are primarily where the differences are with 1071.

Step 4: Portfolio Level Data Review and Scrub

A new tab for 1071 has been added to our Compliance Monitoring tool. This live functionality enables customers to review and scrub loans across the entire portfolio from a single screen.

Step 5: Generate Compliant Report with Translations

In the Winter Release, Hawthorn River will deliver the final piece of the puzzle, which will be a compliant data extract that is ready to send to the regulatory agency. This data extract will contain all the proper translates based on the CFBP Data Points Chart. The data structure for 1071 will be different from HMDA but the overarching concept will be the same. Other data will flow into the export from information already entered on the application and translations added to the configuration. To exemplify the concept, the following image is from our current HMDA Extract screen.

A Collaborative Effort with TruStage.

TruStage Compliance Solutions has been working with us every step of the way. With direct lines to the CFPB, TruStage brings an excellent perspective on the requirements at both a documentation and process level. This alignment will result in a best-in-class solution that is inclusive of regulatory compliant documentation. The TruStage team will be releasing their supporting documents later this year and we are excited to be one of the first partners to bring the combined solution to market for our valued community bank customers.

In partnership with TruStage, we are closely monitoring the evolving litigation around Dodd-Frank. With many associations and states calling on congress to appeal the ruling, the months ahead will be interesting to say the least. Our joint teams continue to monitor the industry-level angst on this topic and stand ready to make adjustments should they be required. We do not plan to sit idle, however, because it is critically important for our customers to have a trusted solution when it is needed.

Get Started Now.

As we prepare to launch the next iterations of our Dodd-Frank 1071 data collection and reporting solution, we encourage our customers to take the following actions:

Begin familiarizing yourself with the current functionality.

Share feedback with us if we are missing key functionality or if you have an idea how to further streamline the process.

Join our upcoming education webinars, co-hosted with TruStage Compliance Solutions.

Begin drafting your internal procedures and evaluate internal process changes that will be needed (who, what, when).

Let your regulators know you have a plan - get their feedback - share it with us.

Attend the first annual Hawthorn River User Conference (Nov 5-7) to see a live demo of the combined solution!

Hawthorn River is Community Banking Software designed by Community Bankers.

Contact Us to learn more!

Improving Efficiency Ratios With Process Automation

The idea of process automation is a foreign concept to many community bankers. Even for those who are familiar with the term, many struggle to understand the benefits unless they’ve had first-hand working experience with a quality solution.

In short, Process Automation uses a computer to complete work that otherwise would be done manually. When used appropriately, it greatly reduces the amount of effort and time it takes to complete steps within a defined Business Process Flow, yielding higher productivity with lower operating costs.

A great example of Process Automation in Community Banking is the Flood Ordering process.

At many Community Banks, the Flood Report Ordering process starts with either the banker or loan assistant requesting that a flood report be ordered. For internal control purposes, this is commonly (but not always) done by sending an email to the loan processing team – a step that requires information to be keyed about the property and order requirements into the email. Next, the person responsible for completing the order will connect to the flood provider’s website and re-key the information for the order. The order is then processed by the flood company and the flood report is made available to the requesting employee. The requesting employee will then often times update a log and send the order form back to the banker. The banker will then update any relevant information on the application (yes, that’s the third time we have possibly keyed the same data). The flood report is then stored in the file, which for many remains a physical file (a critical topic for a future post). If needed, the banker (or someone on the team) forwards the flood report to the borrower. With all of the handoffs in the process, this simple request can take hours (if not days to complete).

How does Process Automation Help?

By leveraging Process Automation, a majority of the Floor Report ordering work described above is shifted to the LOS. During the initial application process, the LOS captures all of the relevant information that is required to complete the Flood Order, including the property address and borrower details. This information is passed by the computer to the the third party flood reporting firm at a click of a button. The request is automatically processed by the flood reporting firm and an electronic version of the Flood Report is returned to the banker. At this point, the LOS automatically logs the request, updates the relevant information, notifies the interested parties, and stores the document in the file repository. All of these steps are completed in about 10 seconds with process automation.

Similar to the Flood Order example, an LOS can be leveraged to effectively automate many of the lending processes within a Community Bank. Some examples include:

· Appraisal Bidding

· Appraisal Ordering

· Credit Report Ordering

· Disclosure Delivery

· Loan Renewals

· Title Report Ordering

· Tickler & Exception Management

Ultimately, Process Automation can greatly reduce the amount of human labor required to get work done. This can help a Community Bank scale more efficiently over time, ultimately driving down the Efficiency Ratio.

It’s important to note, however, that Community Banking is about relationships, not technology. Even though technology plays a vital role in shaping how we get work done, technology is nothing more than a tool in the toolbox that should ultimately be leveraged to drive improved client relationships. Too often, technology gets in the way rather than supports our efforts as Community Bankers. Process Automation, when leveraged correctly, can be an effective tool in the toolbox that greatly improves productivity and yields stronger client relationships.

Hawthorn River is Community Banking Software designed by Community Bankers.

Contact Us to learn more!

Workflow Engine - The Brains of the Loan Origination System

Community bankers face a growing challenge in driving profitably. Net interest margins are believed to be permanently tightened and our big-bank counterparts possess a 10% - 20% advantage when it comes to efficiency ratios. This leaves us with a real need to examine how we get better at playing the game. One strategy that community bankers can deploy is to leverage workflow technologies as part of an overall Loan Origination Solution to drive material improvements to the cost of delivery.

Before diving into details about the Workflow Engine, lets first define a Business Process Flow. For simplicity, I like to think of a Business Process Flow as an Assembly Line. Much like a physical manufacturing company produces widgets through a series of manufacturing steps, Banks produce services by moving information through a series of processing steps - this is a bank’s assembly line. In the case of lending, information such as the customer’s financial statement, business objectives, and desired deal terms serve as the “Raw Materials". These Raw Materials are systematically transformed into a funded loan by completing a series of defined processing steps.

A Business Process Flow for Community Bank Lending looks something like this…

There are three inherent challenges that Community Bankers face when managing the Business Process Flow for their lending activities.

Information Overload - The amount of information required to “manufacture” a loan is significant (and continues to increase). The type of information that must be collected also varies greatly based on the structure of the loan, borrowers, and collateral. As regulations evolve, so does this complexity. As a result, Bankers often key (and re-key) unnecessary information and find that they are missing required information at the time of closing. This isn’t the fault of the banker – it’s a breakdown in the assembly line tools.

Lack of Visibility – Community bankers work on multiple loan deals at once. These deals are at varying stages of the lending process flow and therefore have different team members responsible for completing the process step. Keeping track of all the loans in process becomes increasingly difficult with volume. Time is wasted by the banker with phone calls and emails to track down information about the loan status and borrowers are negatively impacted by this lack of transparency.

Activity Management – The amount of time and effort it requires to complete a business loan is staggering. There are a multiple hand-offs that take place during the process flow and the number of detailed processing steps within each department is significant. Most Community Banks have attempted to tame this chaos with manual checklists but the challenge is becoming too great for manual solutions.

Addressing these business challenges is where the Workflow Engine shines! Functioning as the brains of the LOS, the Workflow Engine orchestrates the entire Business Process Flow for the banker. It serves as the helping hands to let the banker know exactly where their loans are within the process and what needs to be done in order to move the loans forward. It keeps up with regulatory changes and information requirements so that the right information is entered at the right time. The Workflow Engine also manages the approval processes and automates activity management with proactive actions such as task assignment, report generation, and borrower notifications. The end-result is substantially improved credit quality, productivity, and client satisfaction.

Functioning as the brains of the LOS, the Workflow Engine orchestrates

the entire Business Process Flow for the banker

The Workflow Engine is responsible for executing a number of independent functions at one time while also ensuring all of the functions are working together in a seamless fashion. With an effective Workflow Engine in place, the Community Banker is able to spend less time tracking down information and more time with clients.

The top 5 features offered by the workflow engine include:

Dynamic Screens - As noted above, time is often wasted keying information about a loan that doesn’t even apply. Dynamic screens are used by the workflow engine to present the banker with intuitive and clear input points that adjust dynamically based on the structure of the loan, borrowers, and collateral. Therefore, you are only asked to enter the information that is relevant to the loan.

Field & Document Validations - With the vast amounts of information being collected during the loan origination process, it’s extremely challenging to know what information is required at each stage of the process. Field & Document Validations are leveraged to help bankers know when specific information is a "nice to have” or a “need to have”. Examples include requirement of an Interest Rate prior to approval or the requirement of a flood letter before documentation. These validation rules will also vary based on the structure of the loan, borrowers, and collateral. The end result is improved data quality and less rework for everyone involved.

Approval Routing & Signature - Each Community Bank has a unique set of policies governing their loan approval process. The Workflow Engine can assist the banker through the approval process with intelligent approval routing and online approval capabilities based on the loan structure. including both signature and committee based approvals.

Unique Workflows - Much like manufacturing has different assembly lines for the production of standard widgets versus custom widgets, bankers need the ability to produce loans under different Business Process Flows. A consumer loan, for example, should have a flow that is quick and minimally customized. A complex commercial credit, on the other hand, may require an extended flow with more customization abilities. The Workflow Engine should be leveraged to support this variance in order to optimally move all of the loans through the process.

Process Automation - Process Automation enables bankers to be more productive by reducing the effort and time it takes to complete the Business Process Flow. The Workflow Engine delivers these benefits by shifting work from the employee to the computer. This may be something as simple as assigning a follow-up action item to a team member at a specified time or a more complex activity such as automatically notifying a borrower that their financial statement is about to expire.

In this post, we discussed the challenges that Community Bankers face when managing the lending Business Process Flow. We then outlined how the Workflow Engine (The Brains of the LOS) serves as the helping hands to the banker in order to overcome the inherent challenges of the lending “assembly line”. We concluded with five specific Workflow Engine features that directly improve the productivity of the banker, the quality of the data, and the experience of the client.

Contact Us to learn more!

Hawthorn River is Community Banking Software designed by Community Bankers.

Why Community Bankers Need a Loan Origination System

In a industry that is rapidly consolidating, community bankers face continual pressure to become more efficient. The good news is that most community banks haven’t scratched the surface when it comes to driving meaningful productivity improvements in their lending process. Since lending serves as the bank’s primary revenue driver, incremental improvements in the cost of loan delivery can have massive returns on the income statement.

The big banks figured out how to systematize their lending process long ago and are now realizing the benefits on their bottom line. Until recently, many of these Loan Origination Systems (LOS) technologies were out of reach to the community banks due to cost and complexity. But thanks to the advancement of cloud computing and the re-emergence of Fintech solution providers, such as Hawthorn River, community banks have a chance to level the playing field.

For the purpose of this discussion, Loan Origination System (LOS) is defined as the software that manages the end-to-end processing steps that occur from the time of a borrower request to the time of funding. This includes activities such as the loan application, credit underwriting, approval, documentation, closing, and booking. While these steps may vary slightly based by bank, they a representative of most common LOS activities.

Today, many Community Banks rely on a patchwork of disconnected tools and communication channels to support the loan origination process. The standard tools of the trade include Word, Excel, Emails, and Phone Calls. As a result, bankers often wrestle with a tedious process for each and every loan they originate (including all those pesky renewals). Bankers have limited visibility into their loans in process and find themselves (or someone on their team) re-keying data multiple times along the way. While time tested for decades, this manual approach to loan origination is increasingly difficult to sustain as regulatory complexity increases, borrower expectations transform, and operating margins tighten. These problems compound with growth and the constant changes in regulations.

Loan Origination Software attacks these challenges head-on by delivering systematic workflows to guide bankers through the process of originating the loan. Rather than re-keying data into multiple tools, an effective LOS allows the banker to enter data one time and then flow this data through the process. An LOS also reduces regulatory complexity by proactively identifying potential triggers and requiring specific actions to be taken, such as the delivery of a disclosure to a borrower. In addition, the training and on-boarding of new employees is greatly simplified by leveraging an LOS since the bank can provide tools to the banker that allows them to be more productive while and better positioned to manage regulatory risks.

Hawthorn River helps community banks streamline lending by automating manual tasks, proactively monitoring compliance, and standardizing unruly and chaotic processes.

Contact Us to learn more!

Hawthorn River is Community Banking Software designed by Community Bankers.